Living and working in today’s environment involves many risks. Risks can be viewed as threats, but business exists to cope with risks. No one should expect compensation or profit without taking on some risk. The key to successful risk management is to select those risks that one is competent to deal with, and to find some way to avoid, reduce, or insure against those risks not in this category. Risk represents a combination of the systematic risk and unsystematic risk, including potential internal and external threats and liabilities. Total risk is the sum of systematic and unsystematic risk. Value at risk (VaR) is an attempt to provide a single number that summarizes the total risk in a portfolio.

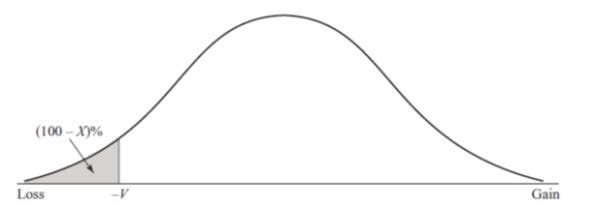

The variable V is the VaR of the portfolio. It is a function of two parameters: the time horizon, T, and the confidence level, Xpercent. It is the loss level during a time period of length T that we are X% certain will not be exceeded.

VaR is an attractive measure because it is easy to understand. It asks the simple question “How bad can things get?” This is the question all senior managers want answered. However, it doesn’t answer, what will be the loss being greater than Xth percentile of the loss distribution?

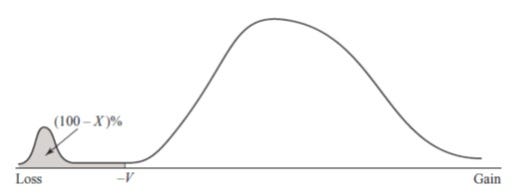

Expected tail risk (ETL), sometimes referred to as conditional value at risk, asks the question: “If things do get bad, what is the expected loss?”

Expected shortfall, like VaR, is a function of two parameters: T (the time horizon) and X (the confidence level). It is the expected loss during time T conditional on the loss being greater than the Xth percentile of the loss distribution.

Measuring tail risk is a central component of risk management systems and the basis for the

determination of capital requirements. However, Managers ignore them too often, whether to save money or avoid planning for a highly unlikely occurrence and undervalue future risk. Ignoring these extreme risks may threaten the continuity or sustainability of an organization.

After the turn of the millennium, several giant corporations experienced avoidable disasters exposing flawed risk management processes. When a tsunami hit, destroying three of Fukushima’s nuclear reactors, one of the world’s largest nuclear disasters unfolded. Although Fukushima could not have prevented the tsunami, but its means of protecting its equipment from such event was far from enough. Had Fukushima Daiichi planned well for the unlikely tail risk, it might have avoided catastrophe.

If these risks are so perilous, why do they continue to go undetected by managers?

Cognitive biases, including overconfidence, anchoring, and group-think, get in the way of objective decision making. While it might not be possible to monitor all potential risks and mitigate them. Managers need to address two key issues: how to best manage the tail risks, and whether such tail risks can be reduced effectively at a reasonable cost.

Planning for tail risks may be costly up front, but as seen with Fukushima, underestimating tail risks can be hazardous to an organization. The first step is to align with best practices and improve communications when it comes to recognizing risks. Once communication is improved, a systematic approach to monitoring risks can reduce the likelihood of ignoring them, enhance information and improve decision making.